By Alex Tarrant

KiwiSaver withdrawals could be taxed once a person hits 65, with that revenue diverted back into the New Zealand Superannuation Fund to manage future New Zealand Superannuation costs, former Labour Party Finance Minister Michael Cullen says.

Other ways of managing looming super costs due to New Zealand's ageing population could include a "super levy" paid out from an increase in KiwiSaver contributions, or a form of income testing that would link NZ Super payments to KiwiSaver balances.

Cullen presented the three options for confronting super costs to a Treasury-Victoria University conference on the Government's long-term fiscal projections. He also said it was inevitable the age of eligibility for NZ Super would be raised from 65 to 67, and that it wasn't too long a shot that KiwiSaver would soon be made compulsory.

Cullen canvassed the options in this paper presented to the conference (See him speak about them in the video above):

Option one: Link KiwiSaver & NZ Super payments (a form of income testing).

While KiwiSaver may make many more people independent of New Zealand Superannuation, it had no impact on the cost of it, Cullen said.

With the number of KiwiSavers already far higher than forecast, it was not a long step to make the scheme compulsory, tighten some of the criteria, and, over time, gear it up to a level far closer to that planned in Australia.

"At that point the relationship between KiwiSaver and New Zealand becomes one for serious discussion. As an example of what could be considered I have had a number of options modelled," Cullen said.

"The models all start from KiwiSaver becoming compulsory from 1 July 2016 with all people signed up as they turn 18 and the opt-out provision on auto-enrolment removed. All remaining adults would be enrolled on 1 July 2020. The contribution rates would be lifted back to 4% [for employees], and 4% [for employers], also from 1 July 2016. Employer contributions would then increase by 0.5% per annum until reaching either 8% in one set of models or 6% in the other," he said.

"As a matter of practicality and individual affordability it may be desirable to begin new entrants on a lower personal contribution rate, say 2%, and gear up over time, but as this has no significant impact on costs or effects over the long term it has been ignored in the model runs."

All his runs assumed that, however made up, retired people would continue to enjoy a guaranteed retirement income at least equivalent to that of New Zealand Superannuation based on the current wage relativity formula.

Cullen said two basic ways of reducing the fiscal cost over the long-term of meeting this criterion were explored.

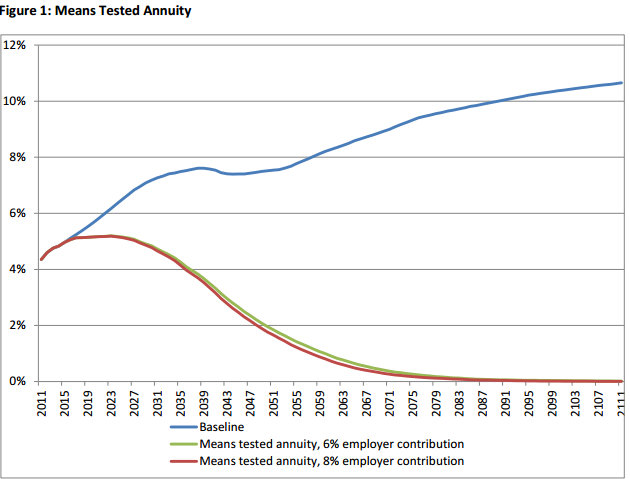

"In the first, it was assumed that half of the accumulated KiwiSaver savings would have to be accessed by way of annuity. Where this was less than the guaranteed retirement income it would be made up to that level," he said.

"In effect this means that for many people the shift from state funding to private funding would result in half of their KiwiSaver savings being income tested away.

"This could prove difficult to establish and maintain as an acceptable policy position even though it certainly has a substantial impact on the long-term fiscal costs. It also has the usual problems of applying an income test fairly," Cullen said.

"However, the fiscal outcomes are impressive. Under either higher contribution rate modelling suggests the cost of New Zealand Super falls to under 2% of GDP by 2050, all but vanishing by the end of the century. Remember, that is based on only 50% of accumulation being taken by way of annuity," he said.

Option two: Tax KiwiSaver withdrawals for Super Fund top up

An alternative which Cullen said would have significant advantages in terms of simplicity and fairness, was to deal with the KiwiSaver/New Zealand Superannuation interface on the revenue side rather than the expenditure side.

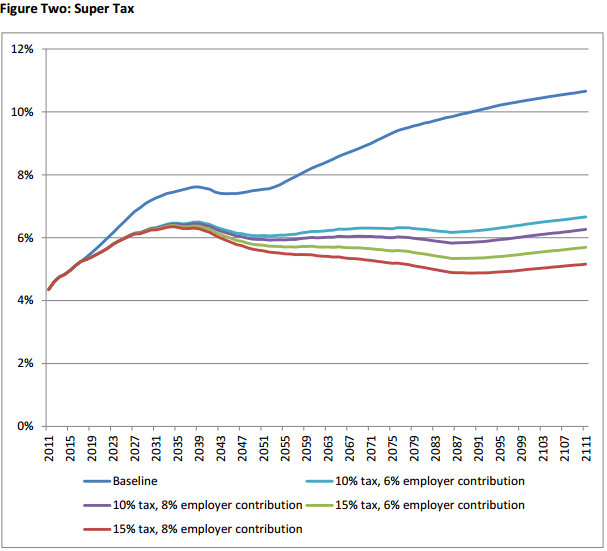

"Under this proposal, the current New Zealand Superannuation scheme would be maintained as is, with the exception of an initial adjustment to the age of qualification to 67 being phased in starting in, say 2020," Cullen said.

"The revenue offset would come from a withdrawal tax on accumulated KiwiSaver savings of either 10% or 15 %. This withdrawal tax would apply to those permanently emigrating or to the accumulated savings at maturity (assumed to remain at age 65). The tax would only apply to accumulations starting with the introduction of the compulsory scheme," he said.

Such a scheme would be administratively much simpler than the first option, avoid the difficulties of income testing, but by the end of this century would reduce the projected net cost of New Zealand Super by about 5% or so of GDP, having kept that net cost at about 5 % of GDP over the second half of the century.

"Could such a scheme be politically feasible? The answer to that is that anything in this area is fraught with difficulty for obvious reasons. But it does seem to me to have at least as much chance of success as any of the other options that are on the table, either at this conference or elsewhere," Cullen said.

"In order to establish a clear relationship with maintaining the affordability of New Zealand Superannuation two simple things could be done. One would be to name the tax New Zealand Superannuation Tax. The other would be to pay the proceeds of the tax directly into the New Zealand Superannuation Fund," he said.

Option three: Super levy

In his speech, Cullen said he had come up with a third option not canvassed in the paper: part of any increase in KiwiSaver contributions could be paid as a ?Superannuation levy? directly into the Super Fund.

?That?s a form of public saving as you go to offset the future cost of New Zealand Superannuation," Cullen said.

Give govt SOE shares to Super Fund

Cullen also suggested another change which could help secure confidence in the future of New Zealand Super would be to transfer the remaining state asset shares into a holding company owned by the New Zealand Superannuation Fund.

"This would, in effect, bring forward the resumption of government contributions, at a lower rate than previously, but also bring a welcome focus on long term wealth creation with respect to the assets," he said.

pilar sanders andrew young real life barbie zipper armenian genocide asteroid mining memorial day

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.